Polymarket Liquidity, Spread, and Slippage in Telegram Trading

Learn how Polymarket liquidity, bid-ask spread, slippage, market orders, limit orders, partial fills, and failed FAK/FOK orders affect Telegram trading and copy trading.

PolyBot Team

Updated June 1, 2026

Liquidity is one of the main reasons a Polymarket trade can feel different from the price you saw a few seconds earlier.

A market can have a clear headline price, active discussion, and a strong trading idea, but still be expensive to enter if the order book is thin. That is why Polymarket traders need to understand three execution words before they rely on fast buttons: liquidity, spread, and slippage.

If the immediate action is a market buy or market sell, read the Polymarket market orders from Telegram guide before treating the displayed price as the expected fill.

This matters even more after breaking news. Use the Polymarket news trading bot guide when a headline or event update creates urgency before the order book has settled.

The same execution check applies to volume spikes and trending markets. Read the Polymarket volume alerts bot guide before assuming high activity means enough usable depth.

If a Telegram price alert brought you back to a market, use the Polymarket price alerts bot guide to decide whether the current spread and depth still support the trade.

If the order only fills part of the requested size, use the Polymarket partial fills guide to decide whether the smaller position, cancelled remainder, or open order still fits the plan.

If a limit order stays open instead of matching, use the Polymarket limit order not filled guide to diagnose price, spread, depth, queue position, and stale-order risk before retrying.

PolyBot's official Trading Guide describes Telegram flows for paste-to-trade, market buys, selling, limit orders, and order management. Its Market Search Guide also shows that search results expose liquidity, volume, prices, and trade actions. This guide explains how to read those signals before deciding whether to use a market order, a limit order, or no order at all.

For fast-entry workflows, read the Polymarket sniper bot guide before treating speed as protection from slippage.

If a market came from a scanner, trending list, alert, or large-wallet notification, read the Polymarket market scanner bot guide before assuming the displayed price is executable at your size.

For related-market or arbitrage-style trades, this execution layer is the whole trade. The Polymarket arbitrage guide explains how fees, depth, and partial fills can erase a theoretical edge.

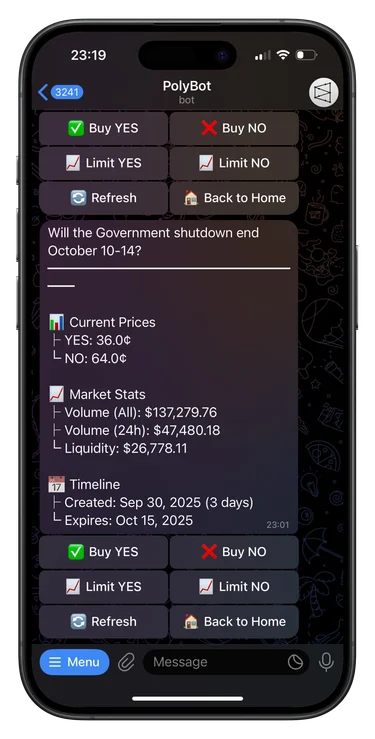

Liquidity means available size at usable prices

Liquidity is not only whether a market has traded before. It is whether enough shares are available near the price you are willing to accept.

A market with high historical volume may still be thin right now if the best orders were filled, cancelled, or moved. A market with visible liquidity may still be poor for a large order if most available size sits far away from the displayed price.

Before trading, ask:

- How much size is available near the current price?

- Is liquidity on the side you want to trade?

- Would your order consume the best price level?

- Does the market still have activity, or is the quote stale?

- Would a smaller order behave differently?

This matters more in prediction markets than many beginners expect. A 10 cent spread in a binary market can completely change the expected value of a trade.

For a focused explanation of bids, asks, depth, and weighted average fill price, read the Polymarket order book guide.

Spread is the first price warning

The bid-ask spread is the gap between what buyers are currently bidding and what sellers are currently asking.

If YES can be sold at 42 cents and bought at 48 cents, the visible spread is 6 cents. A market order to buy YES likely has to cross toward the ask side. A market order to sell YES likely has to cross toward the bid side.

If you are closing exposure, pair this with how to sell a Polymarket position so the exit tool matches the available bid depth.

A tight spread usually means the market has active makers and closer agreement about the current probability. A wide spread can mean uncertainty, low attention, news risk, or simply not enough active liquidity.

For the maker side of that spread, read the Polymarket market making bot guide.

Wide spreads do not automatically mean "do not trade." They mean the market demands a reason. Maybe you have a strong thesis and are willing to post a limit order. Maybe the price is moving fast and immediate execution matters. But you should know which choice you are making.

For the probability and payout side of price reading, read Polymarket odds and prices explained.

Slippage is the gap between expected and actual execution

Slippage is the difference between the price you expected and the price you actually received.

For manual trading, the expected price may be the price shown on the market card. For copy trading, it may be the leader wallet's fill price. For an alert, it may be the price at the time the alert triggered.

Slippage can happen because:

- the market moved before confirmation

- the order book changed after the card loaded

- the order size was too large for visible depth

- another trader consumed liquidity first

- a fast market repriced between signal and execution

- the spread was already wide

Small slippage can be normal. Large slippage can erase the reason for the trade. If a market thesis only has a few cents of edge, a worse fill can turn a good idea into a bad entry.

This is especially important in live sports markets. Read the Polymarket sports trading bot guide before trading game markets from a fast alert.

For fast crypto windows, read the Polymarket crypto trading bot guide before automating entries around BTC, ETH, or SOL moves.

For general fast manual execution, read the Polymarket sniper bot guide before increasing order size.

For how slippage combines with protocol fees, bot fees, gas sponsorship, and funding costs, read the Polymarket trading costs guide. For choosing how much price drift to allow before skipping, read the Polymarket slippage tolerance guide.

Market orders prioritize execution, not the best possible price

A market-style order is built for immediate execution against available liquidity. That can be useful when you need the trade now.

But "market order" does not mean "fill at the displayed price." It means the order attempts to trade through the current book under its execution rules and protection limits.

Polymarket's create order documentation explains that market-style orders use FOK or FAK behavior against resting liquidity, and that the price field acts as a worst-price limit for slippage protection. In practical trader terms:

- FOK means fill the whole order immediately or cancel it.

- FAK means fill what is available immediately and cancel the rest.

- If no matching liquidity exists, the order may fail or skip instead of filling.

That behavior is useful protection. A failed market-style order can be better than a bad fill if the order book no longer supports the trade.

For the full order-type glossary, read Polymarket order types: FOK, FAK, GTC, and GTD.

Limit orders prioritize price, not certainty

A limit order lets you define the maximum price you will pay on a buy or the minimum price you will accept on a sell.

Limit orders are useful when:

- the spread is wide

- you want a specific entry

- the market is thin

- you want to avoid chasing after an alert

- a market order would cross too much spread

- you can tolerate not filling immediately

The tradeoff is simple: better price control, weaker fill certainty.

If the market never reaches your limit, the order may stay open until it fills, expires, or is cancelled depending on the order type. That is why limit orders need review. A good limit order can become stale after news, resolution timing, or a changed thesis.

For the full workflow, read Polymarket limit orders from Telegram.

Why the same market can feel liquid for one trader and thin for another

Liquidity depends on size.

A trader buying $10 of exposure may get a reasonable fill in a market where a $1,000 order would move through several price levels. A copy trading setup with proportional sizing may work at one follower bankroll and fail at another.

For deciding the size before checking the book, read the Polymarket position sizing guide.

That is why a market should not be judged only by whether it has any liquidity. Judge it against the order you plan to place.

Ask:

- Is my order small relative to visible depth?

- Would splitting size reduce impact, or only add delay?

- Would a limit order be more honest about my target price?

- Am I copying a leader whose size already moved the book?

- Does my account size fit the markets this strategy trades?

If the answer is unclear, reduce size or use a limit order until you understand the fill quality.

Copy trading adds a second price gap

Copy trading has two execution layers: the leader's trade and the follower's trade.

If the leader buys at 41 cents and the follower fills at 48 cents, the follower copied the market and outcome, but not the same expected value. That gap can come from latency, liquidity, spread, follower size, or other followers trying to copy the same trade.

PolyBot's Copy Trading Guide describes slippage tolerance as a control over how much drift you accept between the leader's fill and yours. Tight slippage can skip more trades. Loose slippage can fill more trades at worse prices.

For copied wallets, review:

- leader entry price

- follower entry price

- follower order size

- skipped trades

- partial fills

- market category

- spread at copied attempt time

- whether repeated skips are protecting you from bad fills

The copy trading settings guide explains how to configure those controls. The execution speed guide explains how timing affects the follower gap.

If copied trades are skipping repeatedly, use the Polymarket copy trading skipped trades guide to decide whether the skip is price protection, a cap, a filter, or a balance issue.

Search and discovery should include liquidity review

Market search is useful because it helps you find tradable markets faster. It should not turn search results into automatic trade signals.

For alert, wallet, group, and search signals together, read the Polymarket trading signals bot guide before using a fast notification as an order trigger.

When a Telegram market card shows a market, use it as a review surface:

- read the exact question

- confirm YES and NO meaning

- check expiry

- compare displayed prices

- check liquidity and volume

- notice whether the spread is wide

- refresh if the market is live or moving

- choose market or limit order intentionally

High-volume browse modes can help surface markets with more activity, but volume is not the same as current depth at your price. Trending markets can be active and still move too quickly for sloppy execution.

For discovery workflow, read Polymarket market search in Telegram.

Thin-market checklist before you trade

Use this checklist when the market looks thin, volatile, or newly created:

- Re-read the market question.

- Refresh prices if the card may be stale.

- Check the spread before choosing order type.

- Compare your order size with visible liquidity.

- Decide the worst price you will accept.

- Use a limit order if price matters more than immediacy.

- Use smaller size if the order would consume too much depth.

- Avoid retrying failed market orders without checking the book again.

- Review portfolio and open orders after the trade.

- Record whether the fill matched your expectation.

This is not a slow workflow. It is a controlled workflow. Fast execution is useful only when the trade is still worth taking at the executable price.

For automated strategies, apply the same check to every trigger. The Polymarket Auto Trader bot guide explains how slippage, entry windows, and pause rules fit together.

Failed orders can be useful information

A failed order is frustrating, but it can also protect you.

If a FOK or FAK order cannot fill because matching liquidity is gone, the failure tells you the current order book no longer supports the requested trade. That is different from a wallet problem or a broken button.

When a market-style order fails or skips, check:

- best bid and best ask

- available size near your target price

- whether the market moved after you opened the card

- whether your order was too large

- whether a limit order better expresses your intent

- whether retrying would chase a worse price

The Polymarket order failed guide covers balance, allowance, tick size, minimum size, market readiness, FOK/FAK behavior, and other execution errors.

If the failure text points to invalid price precision, use the Polymarket tick size guide before changing spread or slippage assumptions.

Slippage settings are not a substitute for judgment

Slippage settings help define the worst price behavior you are willing to accept. They do not create liquidity.

Tight slippage can protect price quality but increase skips. Loose slippage can increase fills but weaken the trade. Unlimited slippage should be treated carefully because it prioritizes getting into the position over preserving the price reason for the position.

Use stricter settings when:

- the expected edge is small

- the market has a wide spread

- the market is thin

- the leader wallet trades early and size matters

- you would rather miss than overpay

Use looser settings only when you have evidence that the strategy still works after worse fills.

Post-trade review is part of liquidity discipline

The review does not end when the order fills.

After trading, check:

- filled price

- filled size

- average price

- any unfilled amount

- whether an open limit order remains

- whether the position can be exited cleanly

- whether the market is close to resolution

For copied trades, compare your fill to the leader's fill. For manual trades, compare the fill to the price you expected when you confirmed. If the gap is repeatedly larger than expected, reduce size, tighten slippage, use limits, or avoid that market type.

The portfolio and orders guide is the companion workflow for this review.

FAQ

What is a good spread on Polymarket?

There is no universal number. A good spread depends on market volatility, time to resolution, your expected edge, and order size. The important question is whether the spread leaves enough upside after fees, slippage, and exit risk.

Does high volume mean a market is liquid?

Not always. High volume is useful context, but current executable depth matters more for the next order. A market can have historical activity while the current best bid and ask are far apart.

Can a Telegram bot remove slippage?

No. A bot can help you move faster, show confirmations, expose settings, and enforce price limits. It cannot create order-book depth that is not there.

Why did my order fail when the market had a price?

A displayed price does not guarantee enough matching liquidity for your order size and protection settings. The book may have moved, the spread may have widened, or the order type may not have found a match.

Should beginners use market orders or limit orders?

Beginners should learn both. Use market orders when immediate execution matters and the spread is acceptable. Use limit orders when price control matters more than immediate fill certainty.

Trade the order book you have now

Polymarket execution is not only about the market idea. It is also about the order book available when your order reaches it.

Liquidity tells you whether there is enough size. Spread tells you the current cost of immediacy. Slippage tells you how far the final fill moved from expectation. Together, they decide whether a trade that looked good on a card still makes sense at execution time.

Not investment advice. Prediction markets are risky, and liquidity can change quickly.

Polymarket Market Orders From Telegram: Fast Buys, Sells, Slippage, and Risk

How to use Polymarket market orders from Telegram: market buys, market sells, bid-ask spread, slippage, FAK/FOK behavior, partial fills, failed orders, and safer review.

Execution / 11 min

Polymarket Order Book Explained: Bids, Asks, Spread, Depth, and Fill Price

A practical guide to reading the Polymarket order book: bids, asks, midpoint, spread, depth, market buys, market sells, limit orders, fill price, and Telegram trading checks.

Execution / 10 min